The Rural Rundown – Q1 2026 Rural Housing Market Update: Should You Stay, Move, or Buy?

The housing market is still moving, but today’s buyers are doing the math differently.

Focusing on total cost versus price, they’re starting with a monthly number they can live with and then asking what that can get them. This shift is shaping nearly every conversation we’re having with buyers and sellers.

Here’s what’s driving it: the total cost of owning a home has climbed by 80-90% since 2020, and it’s not just because of high mortgage rates. Insurance premiums and property taxes are going up. Energy costs are rising. All while geopolitical concerns are putting a squeeze on spending.

This means affordability pressure on buyers hasn’t gone away. For anyone sitting with the question of whether to stay put or make a move, this is a challenging environment to navigate.

The Rural Rundown from Compeer Home™ serves as a resource to help you understand the market, map out your options, and know where to turn with questions.

In this issue, we provide a data snapshot of today’s market, what it means for you if you’re selling vs. staying, and factors to weigh in the rent vs. buy debate.

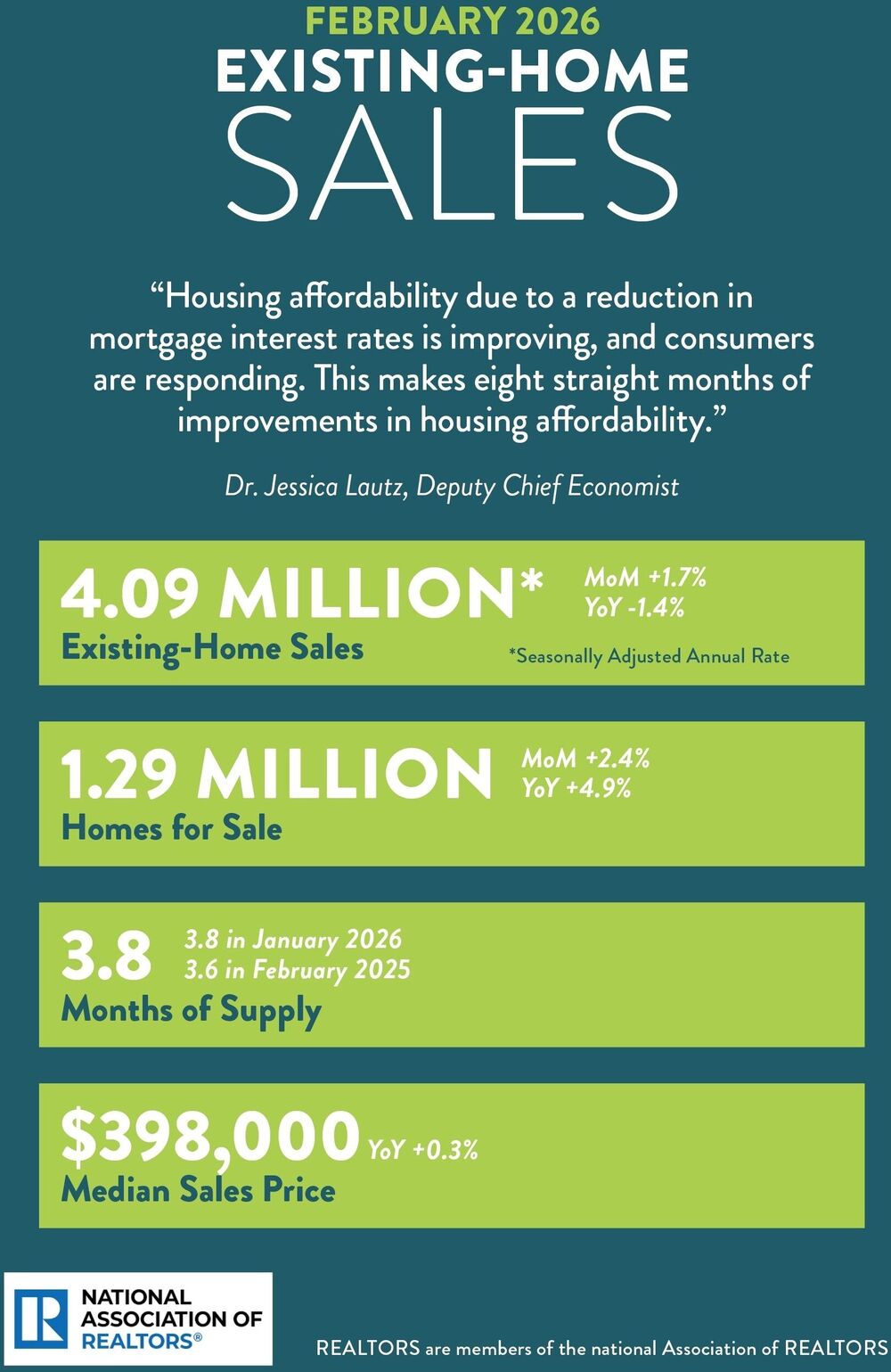

Q1 2026 Housing Market at a Glance

Current Housing Market Conditions: What the Data Shows

The market is starting to level out, but we’re not in recovery yet.

- Existing home sales are up 1.7% month-over-month.

- 1.29 million homes are for sale, with 3.8 months of supply.

- Yet home prices remain near record highs, with a median sales price of $398,000.

- Rural home prices are also up ~60–70% since 2019 (vs. ~30-40% in metro areas), with prices outpacing income by ~2X.

How Mortgage Rates Are Constraining the 2026 Market

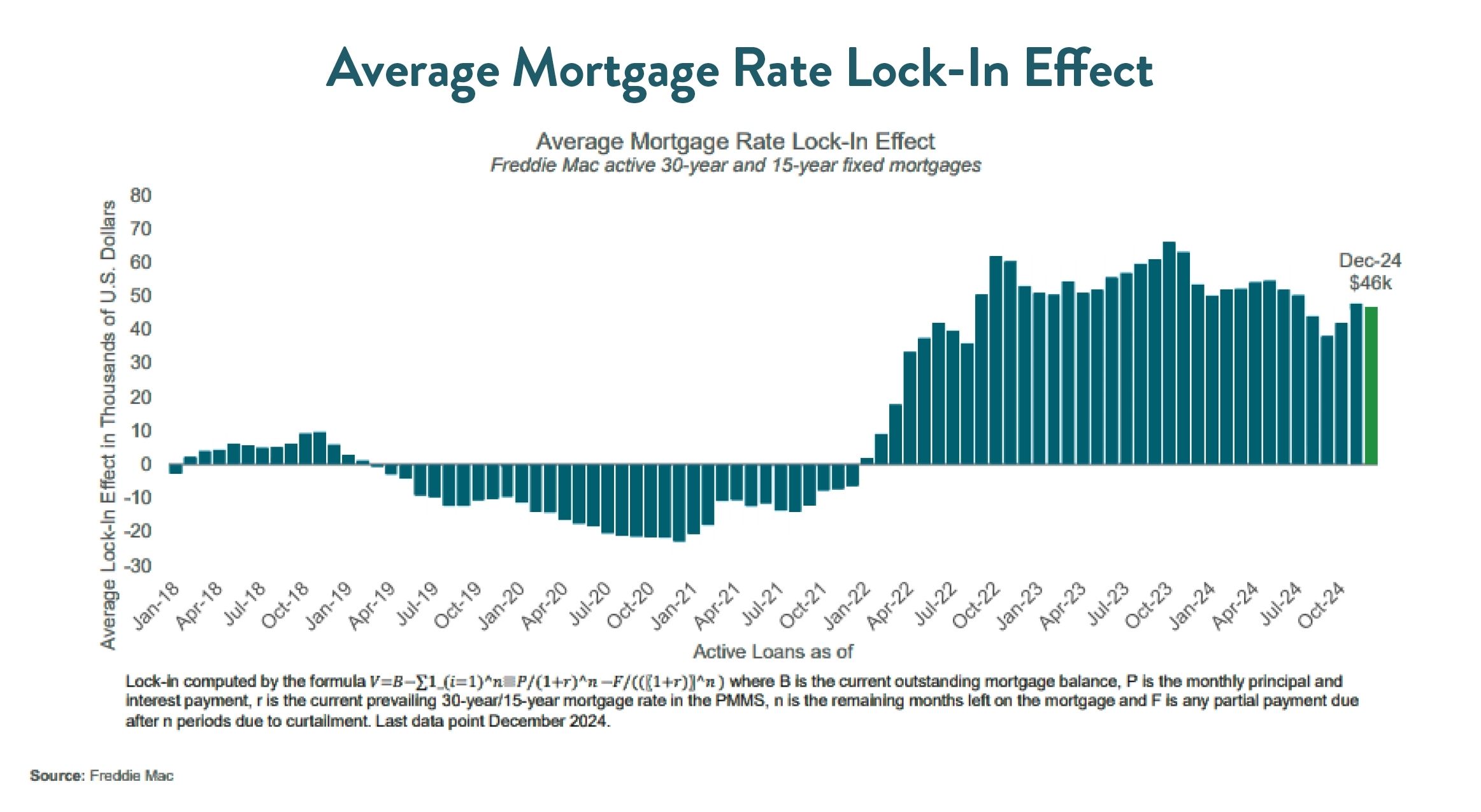

Mortgage rates are still constraining inventory.

- Average 30-year mortgage rate is 6.11%, while 51.5% of outstanding mortgages remain at 4% or below.

- Selling and rebuying today would raise the typical homeowner’s monthly payment by nearly $1,000.

Many rural homes are too old or in too much disrepair to qualify for a mortgage.

- Only 2.9% of rural housing units were built within the last 5 years.

- 450,000+ homes sit vacant due to deterioration, especially concentrated in rural areas where incomes are lower and renovation costs are harder to finance.

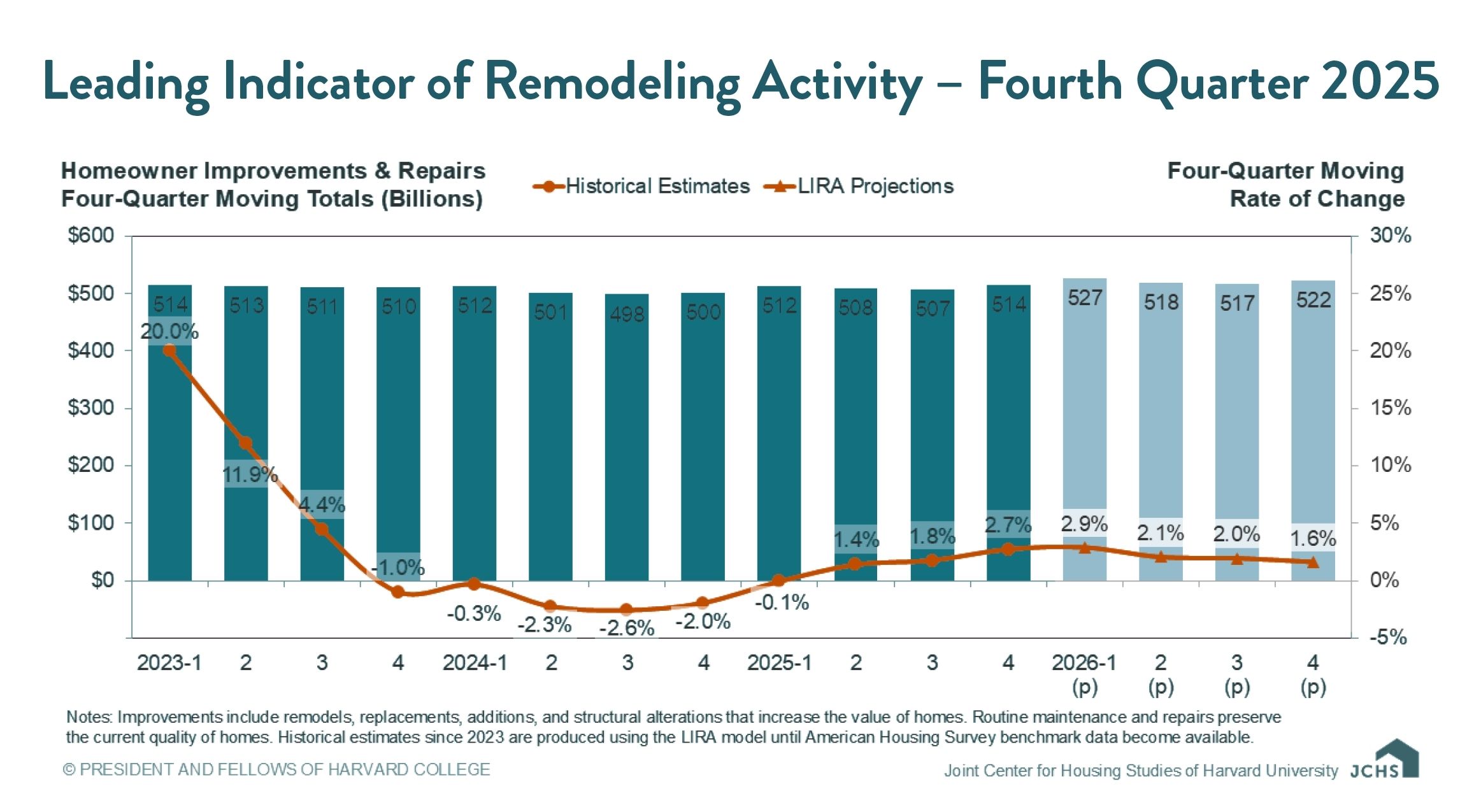

Homeowners Are Remodeling Instead of Moving in 2026

Homeowners are remodeling instead of moving. Remodeling now accounts for ~44–45% of residential construction activity, up from ~33% in 2007.

What the Q1 2026 Housing Market Means for Rural Buyers & Owners

The biggest question we hear right now is ‘what will this cost me every month?’ That’s the right question to ask, as rates are only part of the overall affordability picture. Your mortgage, taxes, insurance, and utilities need to be factored in as well.

Here are some considerations to keep top of mind.

Rural Homeowners: Should You Stay, Renovate, or Move?

The stay-or-move question has no universal right answer. It comes down to your unique goals and financial situation, as well as housing inventory.

39% of U.S. home are owned free-and-clear, with higher concentrations in rural areas, and 54%+ of boomers plan to age-in-place. This not only impacts your choice between staying or buying but also the housing options available to you, should you choose to buy.

Why buy? You might decide to buy if your need have changed. You need a different location closer to family or more land that better fits your lifestyle. Rural properties in particular offer value that’s hard to find elsewhere. If you’ve built equity in your current home, you may also have buying power to leverage.

Why stay? You might stay if you’ve built equity, as selling typically means giving up a mortgage rate and payment you may not be able to replicate. Renovating or updating your current home could also give you more of what you want without starting new financially.

If you decide to stay in your current home, know that your equity can still work for you.

Home equity, the difference between what your home is worth today and what you still owe, can be used for renovations, energy upgrades, debt consolidation, land purchases, education costs, or preparing for larger expenses down the road.

There are two common ways to access it:

- A HELOC gives you flexibility to draw funds as you need them

- A home equity loan gives you a lump sum with a fixed repayment schedule

If you own a manufactured home or a non-traditional rural property, you may still have options. Compeer Home specializes in rural and non-traditional properties and can walk you through what’s available.

Whether you stay and potentially renovate or buy, the decision starts with that same critical question: ‘what will this cost me every month?’ We help you understand your options.

Explore home equity options with Compeer Home.

Thinking About Buying Rural Property in 2026?

Renting feels safer when affordability is tight, but the math isn’t always what it seems. Depending on your situation, buying could cost you less per month, and it builds equity: something renting never does.

Buying a rural property comes with a unique set of considerations, with just a few being:

- Harder-to-finance property taxes, as barndominiums, manufactured homes, and hobby farms don’t fit neatly into conventional loan boxes.

- Trickier appraisals because comparable sales are sparse.

- Non-traditional income nuances, with rural buyers more likely to have farm income, self-employment income, or seasonal income that lenders need to document and underwrite correctly.

That’s where Compeer Home comes into play. Unique rural properties are our specialty, and we live in the same small towns and communities that you’re buying in. We also have first-time homebuyer loans designed specifically for rural buyers.

Explore first-time homebuyer loan options with Compeer Home.

Rent vs. Buy in 2026: What Rural Buyers Need to Know

Deciding whether to rent or buy is one of the biggest financial decisions you’ll make, and in today’s market, it can be a complex choice.

There are tradeoffs for renting and for buying, from upfront costs and monthly affordability to equity and lifestyle. If you’re starting to weigh your options, a clear framework can help ensure you’re considering all factors and asking all the right questions.

This guide breaks down rent vs. buy pros and cons to help you come to the best decision for you: Buying vs. Renting a Home: Should You Buy or Keep Renting? The Pros and Cons of Homeownership

Your Rural Lending Experts

In a market where every dollar of your monthly payment matters, we’re the lender who keeps a pulse on market patterns and trends and knows rural properties inside and out.

What we do at Compeer Home is help you see the full picture clearly, find options you may not know exist, and move quickly on properties that require expertise.

Subscribe now to get more housing market insights, tips and guides from Compeer Home sent right to you.